A Complex Nine Months for a Global Mobility Giant

The first nine months of 2025 present a nuanced picture for the Volkswagen Group—one that blends commercial momentum with financial headwinds, operational recalibration and the early effects of deep structural change. On one side stands a portfolio whose combustion and electric products continue to gain traction across key markets, demonstrating the visible payoff of a multi-year product offensive. In Europe, for example, every fourth electric vehicle delivered during this period carries a Volkswagen Group badge—an unmistakable signal of market relevance in the world’s most competitive EV region.

On the other side, however, sits a financial result weighed down by external pressures, internal realignments and the economics of transitioning to high-volume electric manufacturing. As CFO and COO Arno Antlitz summarises, the Group is operating in a dual reality: solid demand and strong product performance supported by restructuring, yet offset by heavier tariffs, portfolio adjustments and the margin-dilutive effects of scaling lower-margin electric vehicles.

This duality defines 2025 so far—and sets the strategic tone for the Group’s next chapter.

Revenue Growth Amid Shifting Market Currents

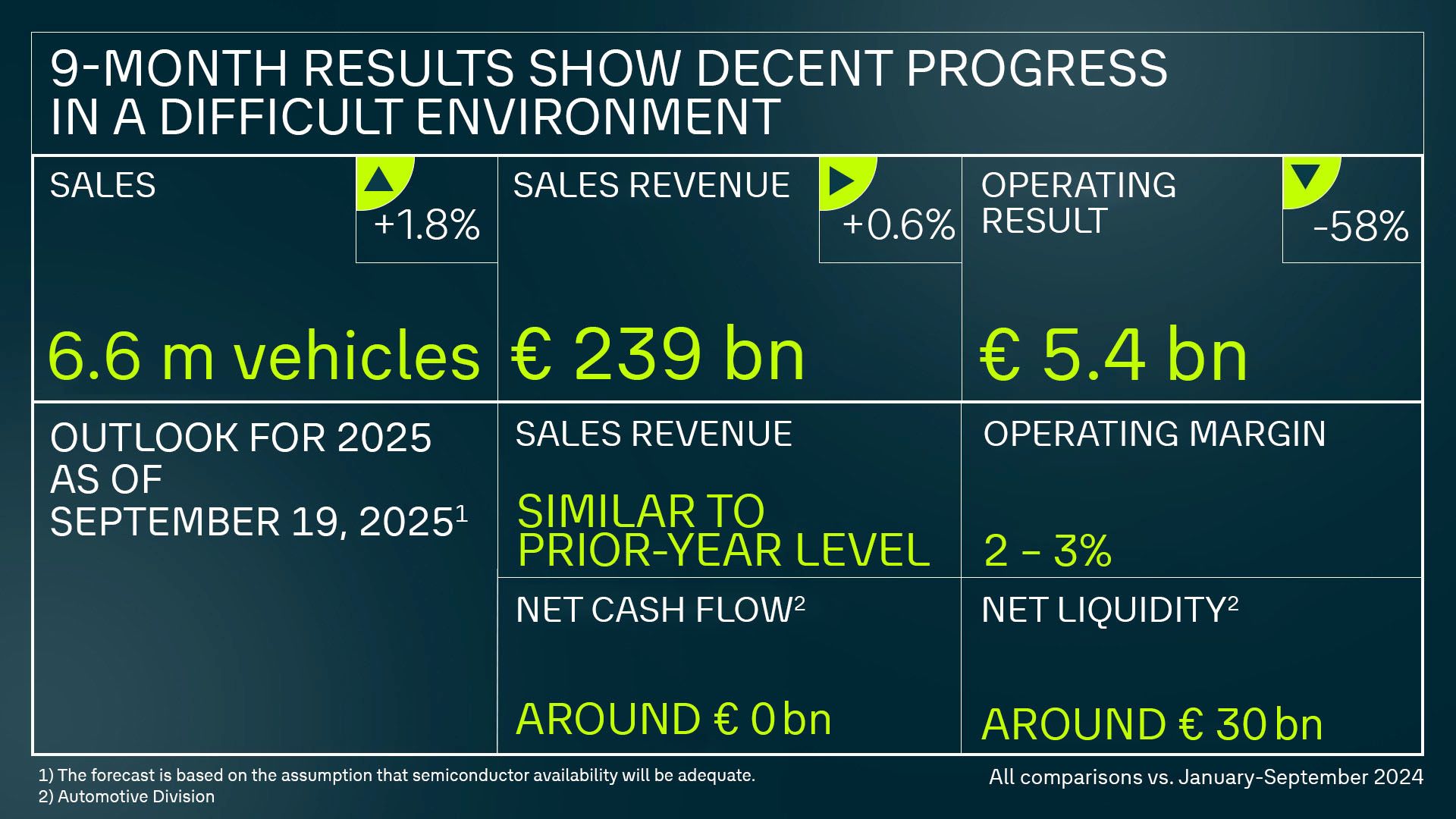

Volkswagen Group generated EUR 238.7 billion in sales revenue in the first nine months of 2025, a slight increase over the prior-year period. Growth from the Core and Progressive Brand Groups more than compensated for the contraction in the Sport Luxury segment, enabling the Group to maintain topline resilience despite uneven global market conditions.

Vehicle sales also tell a story of steady performance: 6.6 million vehicles delivered, up 1.2% year-on-year. Regional dynamics vary considerably—strong surges in South America (+13%), Western Europe (+4%) and Central/Eastern Europe (+11%) offset the expected declines in China (–2%) and North America (–11%). Yet overall, the Group retains its global scale advantage and remains well-positioned to leverage regional pockets of growth.

Crucially, Western Europe’s order intake rose 17%, supported by a 64% surge in battery-electric vehicle orders. This demonstrates both the strength of the product pipeline and the benefit of increasing customer choice across all drive types.

Profitability Under Pressure: Tariffs, Mix and Margin Reality

Where the topline holds, profitability sees meaningful strain. The Group posted an operating result of EUR 5.4 billion, down 58% from the EUR 12.8 billion achieved in 9M 2024, resulting in a 2.3% operating margin. This decline stems from several reinforcing factors: negative price and mix effects, the continued ramp-up of lower-margin EVs, and elevated import tariffs in the United States that are expected to burden results by up to EUR 5 billion on a full-year basis.

The charges recorded during this period—most notably EUR 7.5 billion related to tariffs, Porsche portfolio adjustments and goodwill impairment—further pressure the bottom line. Excluding these charges, the 5.4% underlying operating margin signals respectable performance in a challenging macroeconomic context, yet also quantifies the urgency behind Volkswagen’s performance programs aimed at restoring margin quality.

Cash flow dynamics echo this theme. The Automotive Division posted EUR 1.8 billion in net cash flow, down from EUR 3.4 billion a year earlier, impacted by lower operating cash contributions, US tariff payments and the acquisition of additional Rivian shares. Investment in the future—especially in electrification, software and battery technologies—remains a major cash outflow driver.

Brand Groups: Strengths, Soft Spots and Strategic Pivots

Core Brand Group: Stability Through Discipline

The Core Brand Group continues to display solid financial performance, with a 4.4% operating margin unchanged year-on-year. Increased unit sales and sales revenue offset heavy headwinds from US tariffs and restructuring. Volkswagen Passenger Cars even managed a slight margin improvement to 2.3%, supported by strict cost discipline and the effects of the “Zukunft Volkswagen” program. Škoda remains a pillar of profitability with an 8% margin, while SEAT/CUPRA and Volkswagen Commercial Vehicles experienced declines.

Progressive Brand Group: Revenue Up, Margins Down

Despite higher sales revenue, the Progressive Group’s operating result contracted 26% to EUR 1.6 billion, with margins falling to 3.2%. Tariffs, CO₂ regulation costs and the rescheduling of a D-segment EV platform weighed heavily, signalling the need for renewed efficiency and product cycle optimization.

Sport Luxury: Porsche Realignment Resets the Baseline

The Sport Luxury Brand Group saw one of the most significant swings, with Porsche deliveries down 11% and an operating result of EUR –0.2 billion. This reflects lower Chinese volumes, higher material costs, import tariffs and substantial expenses tied to strategic portfolio realignment and battery initiatives. While the near-term impact is considerable, these measures aim to reposition Porsche for long-term competitiveness in a shifting luxury landscape.

TRATON, CARIAD and Group Mobility: Diverse Performance Across Business Fields

TRATON’s operating result declined 46% to EUR 1.7 billion, primarily due to lower volumes and unfavorable market mix. Meanwhile, CARIAD—still in its transformation phase—reduced its operating loss to EUR –1.5 billion, marking clear progress in software restructuring. Group Mobility emerged as one of the strongest performers, increasing its operating result by 37% to EUR 2.9 billion, demonstrating the margin potential in financial and mobility services.

Strategic Outlook 2025: Efficiency, Synergies and a Reinforced Scale Advantage

Looking ahead, Volkswagen forecasts sales revenue in line with the previous year and an operating return on sales between 2% and 3% for fiscal year 2025. For the Automotive Division specifically, the Group expects an investment ratio of 12% to 13% and roughly break-even net cash flow for the year. Net liquidity is projected at around EUR 30 billion, ensuring strong financial flexibility despite ongoing external pressures.

The broader strategic message is clear: 2025 is a year of consolidation, performance enhancement and structural acceleration. Volkswagen is intensifying its efficiency programs, exploiting Group-wide scale benefits more effectively, and sharpening synergies—especially between platforms, software integration and electrification development.

Adjustments to reporting logic beginning January 2025 will also improve transparency around Automotive Division performance, reducing the apparent investment ratio mathematically by 130 basis points and offering clearer insight into the Group’s capital allocation strategy.

A Transitional Year Guided by Discipline and Determination

Volkswagen Group’s nine-month results reflect the realities of a global automotive leader navigating transformation under pressure. Strong product performance, robust European order momentum and continued strategic restructuring underscore the Group’s inherent resilience. Yet tariffs, margin dilution from EV scaling and significant restructuring charges reveal the depth of the challenges ahead.

Ultimately, 2025 is shaping up as a pivotal year—one where disciplined execution, efficiency measures and a renewed focus on synergies will determine how effectively Volkswagen converts its enormous industrial scale into long-term, sustainable profitability.

The groundwork is being laid. The transformation is underway. And the Group’s ability to act decisively now will define its strength in the decade ahead.